Named drivers, main drivers and fronting: what van owners need to get right

Many van owners are unsure who should be listed as the main driver and how named drivers work. This guide explains the difference, what fronting is, and how to set your van policy up so it reflects real life and protects your cover.

Getting van insurance set up correctly is not just admin. Insurers care a lot about who actually drives the vehicle day to day. If the policy does not match real life, you risk refused claims, cancelled cover, and higher costs in future.

This guide explains what insurers mean by policyholder, main driver and named driver, what fronting is, and how van owners can keep things simple and safe.

Key points at a glance

- The main driver should be the person who does most of the annual mileage in the van.

- A named driver is any other person listed on the policy who is allowed to drive the van, even if they only use it now and then.

- If the person listed as main driver is not the real main user, insurers may treat it as fronting, which they see as dishonest.

- Fronting can lead to refused claims, cancelled policies and trouble getting cover later.

- You should update the policy if who drives the van most of the time changes.

Why main drivers and named drivers matter

When an insurer prices a van policy, they look hard at driver risk. In simple terms they want to know:

- Who uses the van most often

- How far they drive

- What they use it for

If the person at highest risk is not listed correctly on the policy, the insurer is not seeing the real risk. That is where problems start.

Set things up correctly and you stay within the terms of your cover. Get it wrong and you could be accused of fronting, even if you did not set out to do anything wrong.

Key terms in plain English

Policyholder

The person or business that takes out the policy and is responsible for it. On a trade or business policy this could be:

- You as a sole trader

- A partnership

- A limited company

The policyholder is the legal owner of the policy, not always the person who drives the van most.

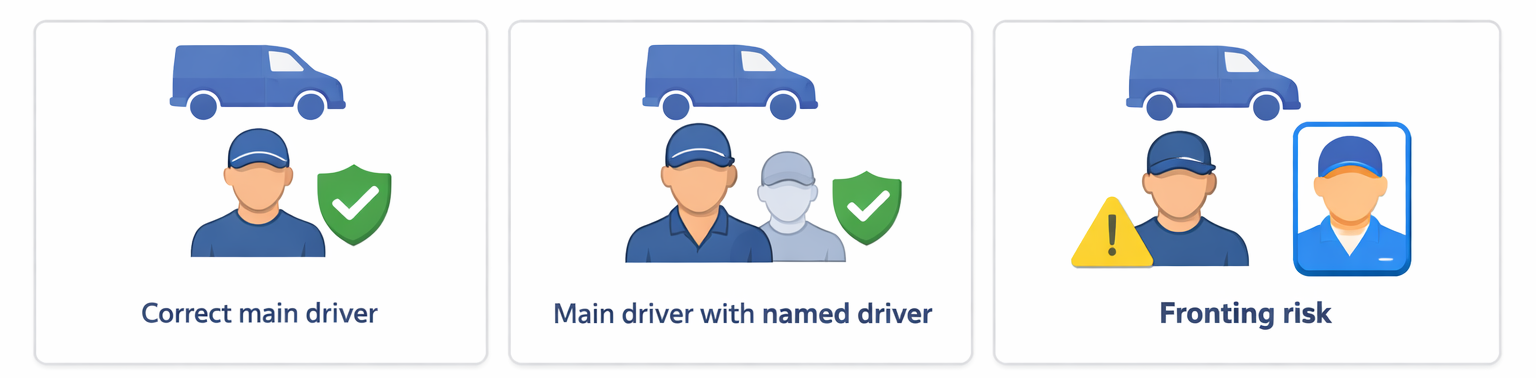

Main driver

The person who uses the van most of the time in real life. That normally means the driver who does the largest share of annual mileage, and often the person who uses the van for work or commuting.

Insurers expect the main driver on the policy to match the main driver in day to day use.

Named driver

Any other person who is listed on the policy and allowed to drive the van.

Some named drivers only use the van now and then, for example:

- Odd weekends

- Holiday trips

- Helping out on the odd job

They are still named drivers on the policy. There is no separate legal label for “occasional driver” on standard van cover.

Fronting

Fronting is when the person listed as the main driver on the policy is not actually the main user of the van, usually to try to keep the premium down by putting a lower risk driver on paper.

Insurers see fronting as a form of misrepresentation and, in serious cases, fraud.

How insurers expect you to set up a van policy

The core rule is simple: the main driver on the policy should match the main driver in real life.

A few common setups make this clearer.

1. Sole trader with one van

- Policyholder: You as the sole trader

- Main driver: You

- Named drivers: Partner or employee who uses the van sometimes

If you do most of the mileage for work, you should be listed as main driver, even if someone else has more years of no claims.

2. Small firm with a “work van”

- Policyholder: The business

- Main driver: The employee who uses the van most days

- Named drivers: Other staff who drive it now and then

If one employee takes the van home, drives to site and does most trips, they should normally be shown as main driver, even if a director owns the van on paper.

3. Family van used for work and home

- Policyholder: One adult in the household

- Main driver: The adult who uses it daily for work or commuting

- Named drivers: Partner or grown-up children who use it at weekends or for odd jobs

Insurers know more than one person may drive the van. They simply want the policy to reflect who is behind the wheel most of the time.

If a named driver is using the van every day for work, their use is no longer “occasional”. In practice they may now be the main driver, and the policy should be updated so it matches that.

What fronting looks like in real life

Fronting is not a formal section in your policy booklet, but it is something claims teams watch for.

Typical patterns include:

- A parent takes out a van policy in their own name and lists themselves as main driver, but their 21 year old child uses it for work every day.

- A business owner lists themselves as main driver to try to keep costs down, but an employee uses the van for almost all site visits and deliveries.

- A friend with a clean record is listed as main driver, while the person who actually uses the van has recent claims or points.

In each case, the insurer is pricing the policy based on the low risk driver, while the higher risk driver is the one using the van most of the time.

Why fronting is a serious problem

If an insurer believes a policy has been fronted, they may:

- Refuse a claim or only pay part of it

- Cancel or void the policy

- Record the issue on shared industry databases

Once that happens, you can find that:

- Future insurance is more expensive or harder to get

- Some insurers refuse to quote at all

- You are treated as having driven without valid cover

If the policy is treated as invalid, driving the van can be treated in law as driving without insurance. That can mean fines, penalty points and even seizure of the vehicle.

Most van owners do not set out to mislead insurers. Problems often come from guesswork, copying what a friend did, or leaving old driver details in place after life changes. It is worth checking your policy now rather than explaining it after a claim.

Common grey areas van owners worry about

“My partner only uses the van at weekends”

If you use the van for work all week and your partner drives it a few times each month, you are still the main driver. Your partner should be added as a named driver if they use it at all, but they should not be listed as main driver.

“My employee sometimes takes the van home”

If the employee is using the van most workdays, they are likely the main driver, even if the policyholder is the business or a director.

If several staff share it fairly evenly, speak to a broker about how to list drivers and mileage so it reflects real use.

“My son or daughter borrows the van now and then”

If it is genuinely “now and then”, they can be a named driver with low expected mileage. If they start using it every day, for example for a regular job, you should contact your broker or insurer to update who is main driver.

The test is always the same: who does most of the mileage over a normal year.

“Can I be main driver on two vans?”

You can be listed as main driver on more than one van, but only if you genuinely use each van more than anyone else does. For most people, work patterns make that unlikely. If another person is doing most of the miles in a particular van, they should normally be shown as main driver on that policy.

How to keep your policy correct and safe

A few simple habits help keep you on the right side of things.

1. Be honest about the main driver

Think about who actually covers the most miles over a full year. List that person as the main driver, even if it costs a bit more at the start. It is cheaper than a refused claim.

2. Add regular users as named drivers

Anyone who drives the van with any regular pattern should be a named driver, not just “in your head”. That includes:

- Staff who often take the van to jobs

- Family members who use it for work or commuting

- Helpers who regularly share longer trips

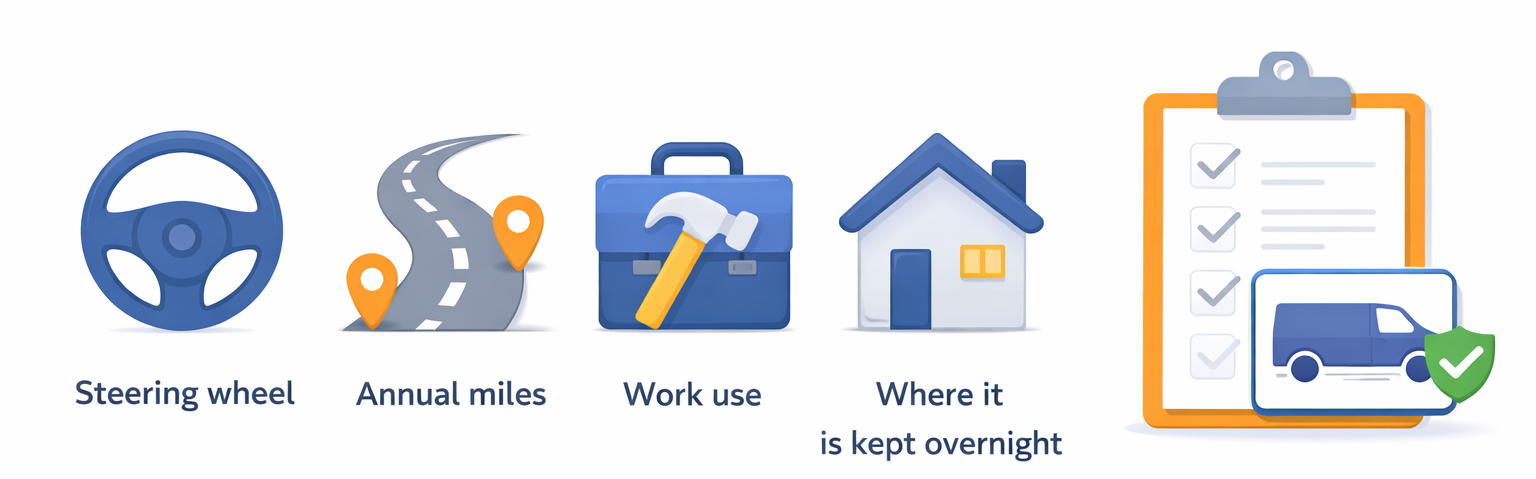

3. Set realistic mileage and use

Be clear about:

- Business use, commuting and social use

- Rough annual mileage

- Whether you carry your own tools, parcels, or just personal items

Your class of use should match what you actually do. If you start doing deliveries when you were only covered for “own goods”, you need to update the policy.

4. Update the policy when real life changes

Good times to contact your broker or insurer:

- New employee starts using the van regularly

- Someone changes role and now drives much more

- You move house or change where the van is kept overnight

- You change what the van is used for day to day

Letting the policy drift away from real life is a common way to end up in a tricky claim.

5. Keep simple records for business vans

For business use, basic notes or job sheets that show who uses each van can help if there is ever a query. Insurers do not expect perfect logs for a one van trader, but clear patterns support your case.

How this works with VanCompare

VanCompare helps you compare van insurance quotes, but the information you enter still needs to be accurate.

When you get quotes through VanCompare:

- You tell us who the main driver is and who the named drivers are

- We pass those details to FCA authorised brokers and insurers on our panel

- They price the policy based on that information and the way you say you use the van

If you are not sure how to set up main drivers and named drivers, you can speak with the broker that handles your policy after you get your quote. It is better to ask a simple question early than argue about a large claim later.

FAQs: main driver, named driver and fronting

1. What is the difference between a main driver and a named driver on van insurance?

The main driver is the person who uses the van most of the time and does the highest share of the annual mileage. A named driver is any other person listed on the policy who is allowed to drive the van, even if they only use it occasionally.

2. Is an occasional driver different from a named driver?

No. An occasional driver is simply a named driver who only uses the van now and then. There is no separate “occasional driver” category on standard van policies, so they are treated like any other named driver.

3. What counts as fronting on van insurance?

Fronting is when the person listed as the main driver on the policy is not the real main user of the van in day to day life. It often happens when a lower risk driver is put down as main driver to try to keep the premium down, while a higher risk driver actually uses the van most of the time.

4. What happens if my insurer thinks my van policy is fronted?

If your insurer believes your policy is fronted, they may refuse a claim, cancel or void the policy, and record the issue on shared industry databases. That can make future insurance more expensive or harder to obtain, and you could be treated as having driven without valid cover.

5. Can my business be the policyholder and an employee be listed as main driver?

Yes. It is common for the business to be the policyholder and for an employee to be listed as the main driver if they use the van most days. The key point is that the person who does most of the mileage should be listed as main driver, whether they are the owner, a director or an employee.

VanCompare Editorial Team

The VanCompare Editorial Team produces clear, practical insurance guides for UK tradesmen, couriers and small business owners. We work with FCA authorised insurance brokers and use insurer information where relevant to explain insurance topics in plain English and help drivers make informed decisions about cover.